The IRS collected over $98 billion through enforcement actions in fiscal year 2022, according to the IRS Data Book — and the taxpayers who lost the most were not the ones with the biggest debts. They were the ones who waited, guessed, or trusted the wrong process.

Direct Answer

Conventional tax resolution approaches fail because they treat IRS enforcement as a negotiation problem when it is actually a procedural one. The IRS operates on strict timelines, statutory rights windows, and internal protocols that expire without notice. Miss a deadline, respond to the wrong unit, or file the wrong form — and your legal options narrow permanently, regardless of how valid your case is.

Key Takeaways

- IRS collection actions follow a rigid procedural timeline — missing a single deadline can permanently close off your best resolution options

- Responding directly to the IRS without legal representation often resets the clock against you, not in your favor

- Offers in Compromise, installment agreements, and penalty abatement each require different eligibility thresholds — using the wrong tool wastes months

- State tax agencies operate on separate enforcement tracks from the IRS and require parallel action; resolving one does not resolve the other

- Every day of inaction compounds both the financial penalty and the legal complexity — this is not a problem that stabilizes on its own

Why Does Everyone With a Tax Problem Think They Can Handle It Themselves?

There is a persistent belief that owing back taxes is fundamentally a math problem — that if you explain your situation clearly enough, the IRS will understand and work with you. That belief is expensive.

The IRS does not get emotional about collections. It just keeps moving.

IRS Revenue Officers operate under internal guidelines — specifically the Internal Revenue Manual (IRM) — that define exactly what actions they must take, in what order, and on what timeline. They are not evaluating your circumstances with discretion. They are executing a process. When you call the IRS directly, you are not entering a conversation. You are entering their process, on their terms, with their timeline.

The mechanism that makes self-representation dangerous is not complexity — it is asymmetry. The IRS representative knows the procedural map. You do not. Every response you give either opens or closes doors you cannot see.

What Is the Real Problem — and Why Is It Not What Most People Think?

Most people frame their tax problem as a debt problem. The real problem is a rights-erosion problem.

Rights-erosion is the process by which legally available resolution options expire or become inaccessible due to missed procedural deadlines, improper responses, or inaction during critical IRS notice windows.

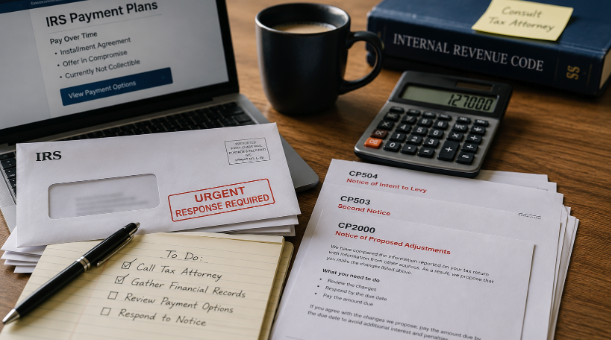

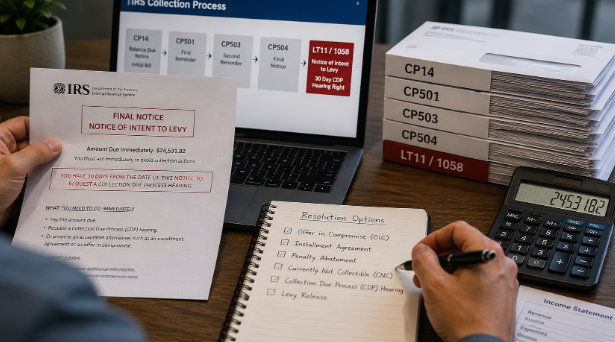

The IRS issues a sequence of notices — CP14, CP501, CP503, CP504, and ultimately the Final Notice of Intent to Levy (Letter 1058 or LT11). Each notice in that chain carries a specific response window. The Letter 1058, for example, triggers a 30-day window to request a Collection Due Process (CDP) hearing — one of the most powerful legal tools available to stop a levy. Miss that window and the CDP right converts to a weaker “equivalent hearing” that does not suspend collection activity.

Most people do not know this. Most people throw the letter in a drawer.

The IRS does not penalize you for ignorance — it simply proceeds as if you agreed.

That is not a metaphor. Under IRS procedure, failing to respond is treated as acquiescence. The enforcement machine does not pause to ask whether you understood the notice. It advances.

Why Does the Conventional Approach Keep Failing the Same People?

The root cause is structural, not behavioral. Conventional tax resolution — whether through DIY attempts, non-attorney tax services, or generic payment plans — fails because it addresses the symptom (the balance owed) without engaging the procedural infrastructure that controls what resolution options are still available.

Here is the specific mechanism: IRS enforcement operates across multiple functional units — Automated Collection System (ACS), Revenue Officer field assignments, the IRS Independent Office of Appeals, and the Tax Court. Each unit has different authority, different timelines, and different leverage points. A resolution strategy that works with ACS is often the wrong strategy once a Revenue Officer is assigned. Treating them as interchangeable is one of the most common — and costly — mistakes tax resolution firms make.

Non-attorney tax services frequently use a one-size-fits-all approach because they lack the legal standing to escalate into Appeals or Tax Court. That limitation is rarely disclosed to clients upfront. Understanding what a tax attorney actually does that general advice leaves out is often the first step toward realizing why that distinction matters so much once a case escalates.

The Procedural Leverage Framework: A Tool for Diagnosing Where You Actually Stand

The Procedural Leverage Framework is a diagnostic tool for identifying which IRS resolution pathways are still open based on where a taxpayer currently sits in the enforcement sequence.

It works across four stages:

| Stage | IRS Status | Available Options | Urgency Level |

| 1 — Notice Phase | CP14 through CP503 | Full range: OIC, IA, CNC, penalty abatement | Moderate — act within 60 days |

| 2 — Final Notice Phase | CP504, Letter 1058/LT11 | CDP hearing, levy release, installment | High — 30-day hard deadline |

| 3 — Active Collection | Levy issued, garnishment active | CDP equivalent, levy release, hardship | Critical — same-day action possible |

| 4 — Revenue Officer Assigned | Field RO contact made | Negotiated resolution, Trust Fund analysis | Critical — every interaction is documented |

Use this framework when: you have received any IRS notice and are unsure what it means or what to do next.

Do not use this as a substitute for legal analysis — it is a triage tool, not a resolution strategy.

What Actually Works — and What Realistic Outcomes Look Like

Effective tax resolution is not about finding a loophole. It is about engaging the IRS procedural system with the right legal tools, at the right stage, before options expire.

McCauley Law Offices uses a proven 4-step process: stop collection actions immediately, investigate the full scope of the tax liability, negotiate the best possible resolution, and deliver a final outcome that leaves clients tax-compliant. That sequence matters because each step unlocks the next — you cannot negotiate effectively while a levy is actively draining a bank account.

Realistic outcomes depend heavily on timing and financial profile:

- A self-employed contractor who had accumulated $87,000 in back taxes over four years, including trust fund penalties, resolved the liability through a combination of penalty abatement and an installment agreement — reducing monthly exposure by more than 60% and avoiding a wage garnishment that had already been initiated.

- A small business owner facing a $1.2 million IRS assessment resolved to $27,000 through an Offer in Compromise — a result that required precise financial disclosure, correct form selection, and Appeals-level negotiation that a non-attorney service could not have accessed.

Timelines vary. An Offer in Compromise typically takes 12 to 24 months to process. Levy releases can happen within days when the right documentation is filed. The single most important variable in any resolution is how much procedural runway remains when representation begins. The real ROI of hiring a tax lawyer, honest timelines, and what drives the difference in outcomes often comes down to exactly that window of time.

> The difference between a $27,000 settlement and a $1.2 million liability is not luck — it is knowing which door to open before the others close.

How Does Tax Resolution Through an Attorney Compare to Other Options?

Not every path to resolving back taxes is equal. The tradeoffs are real and worth understanding before you choose.

| Approach | Legal Standing | Can Access Appeals/Tax Court | Handles State + Federal | Typical Cost Range |

| DIY / Self-Representation | None | No | Rarely | Low upfront, high risk |

| Enrolled Agent | Limited | No | Sometimes | Moderate |

| CPA | Limited | No | Sometimes | Moderate |

| Non-Attorney Tax Firm | None | No | Sometimes | Moderate — variable |

| Tax Attorney | Full | Yes | Yes | Higher — but legally protected |

The critical distinction is legal standing. Only a licensed tax attorney can represent you in IRS Appeals, Tax Court, or in criminal tax matters. If your case escalates — and unresolved cases frequently do — a non-attorney representative has to stop at the door.

McCauley Law Offices holds direct access to IRS Appeals and operates across all 50 states, including parallel state tax resolution — which matters because state agencies do not wait for federal resolution to proceed with their own enforcement.

Who Is This Approach Not Right For?

Honest answer: legal tax resolution is not the right fit for everyone.

If your total tax debt is under $5,000 and you have no collection actions pending, a direct payment arrangement through IRS.gov may be sufficient. If you have already received a favorable installment agreement and are current on payments, there may be no reason to reopen the case.

Legal representation does not guarantee a specific outcome. An Offer in Compromise is not available to every taxpayer — the IRS rejects a significant portion of OIC applications, often because the applicant does not meet the financial eligibility threshold or the submission was incomplete. Representation improves the odds and protects your rights. It does not override IRS eligibility criteria.

> If someone promises to settle your tax debt for “pennies on the dollar” without reviewing your financials first, that is a sales pitch — not a legal assessment.

FAQ: Real Questions From People Who Are Actually in This Situation

Can the IRS really garnish my wages without warning? Not without a process — but the warning comes in the form of IRS notices most people ignore or misread. Once a Final Notice of Intent to Levy is issued and the 30-day response window passes without a CDP request, the IRS can proceed with wage garnishment. At that point, stopping it requires immediate legal action, not just a phone call.

What is an Offer in Compromise and does it actually work? An Offer in Compromise is an IRS program that allows eligible taxpayers to settle their tax debt for less than the full amount owed, based on their ability to pay, income, and asset equity. It does work — but IRS acceptance rates are selective, and an incomplete or incorrectly filed application is typically rejected outright. Working with a tax attorney significantly improves submission quality and outcome.

If I set up a payment plan, does that stop the IRS from taking my assets? A standard installment agreement does not automatically release existing liens, and it does not prevent new liens from being filed. It does generally pause active levy action while the agreement is in effect — but only if you remain current. One missed payment can restart the entire enforcement sequence.

How long does it actually take to resolve a tax problem? It depends on the resolution path. A levy release can happen in days. An installment agreement typically takes weeks to finalize. An Offer in Compromise takes 12 to 24 months on average from submission to IRS decision. The sooner representation begins, the more options remain available — and the shorter the overall timeline tends to be.

What happens if I just ignore the IRS notices? The IRS proceeds. Ignoring notices does not pause the enforcement timeline — it accelerates it. Liens are filed, levies are issued, and resolution options expire. Practitioners consistently observe that the taxpayers with the fewest remaining options are those who waited the longest to act.

Will hiring a tax attorney make the IRS come after me harder? No — and this is one of the most persistent misconceptions. Retaining legal representation triggers specific IRS protocols that require the agency to communicate through your attorney, not directly with you. It does not escalate scrutiny. In most cases, it immediately reduces the direct pressure on the taxpayer.

I owe taxes in multiple states as well as to the IRS — can one attorney handle all of it? State tax agencies operate on separate enforcement tracks and have their own collection tools, timelines, and resolution programs. A tax attorney who handles multi-state matters — like McCauley Law Offices, which operates across all 50 states — can coordinate federal and state resolution simultaneously, which matters because resolving one does not pause the other.

If You Are Reading This and the IRS Has Already Started Moving, the Time to Act Is Now

The IRS does not wait for you to feel ready. Every notice that goes unanswered, every deadline that passes, narrows the legal space you have to work with.

If you have received IRS notices, have a wage garnishment in place, or are watching a bank account get drained — call McCauley Law Offices today for a free, risk-free case evaluation. You will speak with a tax attorney who will tell you exactly where you stand, what options are still open, and what needs to happen first to stop the IRS in its tracks.

Do not hand over another dollar or another day without knowing what you are actually entitled to.

Call McCauley Law Offices or visit mlotax.com to get your case evaluated — before the next deadline closes another door.

References

IRS Data Book — annual IRS publication covering enforcement statistics, collections, and audit activity by fiscal year.

Internal Revenue Manual (IRM) — the IRS’s official internal procedural guide governing Revenue Officer conduct, notice sequences, and collection timelines.

IRS.gov — official source for Offer in Compromise eligibility criteria, Collection Due Process hearing rights, and installment agreement programs.