Direct Answer

IRS defense feels harder than it should because the system is designed for compliance, not resolution — and most taxpayers approach it without understanding the procedural windows that control their options. The right intervention, at the right stage, stops collections, releases liens, and opens negotiation pathways. Waiting closes those windows permanently.

Key Takeaways

- Every IRS enforcement action has a procedural deadline — missing it eliminates legal options that cannot be recovered.

- Responding to IRS notices without a tax attorney often accelerates enforcement rather than slowing it.

- The IRS has specific programs (Offer in Compromise, Currently Not Collectible, Installment Agreements) with qualifying criteria — not everyone qualifies for every program.

- A lien and a levy are not the same thing: a lien is a legal claim on your assets; a levy is the actual seizure of them.

- Most people who try to resolve tax debt alone spend more money and more time than those who hire representation immediately.

Why Does IRS Defense Feel So Much Harder Than the Debt Itself?

The tax debt is the number. The IRS enforcement system is the maze.

Most people who owe back taxes aren’t dealing with a simple bill. They’re dealing with a bureaucratic enforcement mechanism that operates on its own timeline, communicates in dense statutory language, and does not pause while you figure out what to do. The IRS does not get emotional about collections. It just keeps moving.

The core problem isn’t the amount owed — it’s the procedural gap between what the IRS sends and what the taxpayer understands.

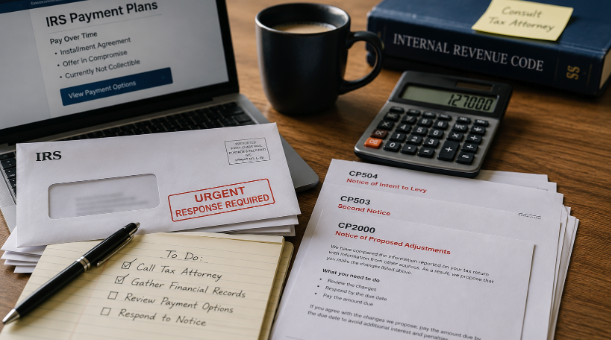

When a CP2000 notice arrives (a notice proposing changes to your return based on mismatched income), most recipients either ignore it or respond defensively without knowing that a CP2000 is not a bill — it’s a proposal. Responding incorrectly can convert a negotiable discrepancy into an assessed liability with penalties attached. That one misstep can add thousands to a debt that didn’t have to exist.

> The IRS enforcement system isn’t punishing ignorance on purpose — it’s just indifferent to it. That indifference is what makes professional representation the difference between resolution and escalation.

What’s the Real Root Cause — Why Does This Keep Getting Worse?

The systemic reason IRS problems compound isn’t procrastination. It’s procedural invisibility — the taxpayer cannot see the enforcement timeline the IRS is operating on.

Procedural invisibility is the condition in which a taxpayer receives IRS communications without understanding the internal enforcement sequence those communications represent. Each notice is a step in a predetermined escalation chain. The taxpayer sees paper. The IRS sees a clock.

Here’s what that looks like in practice: A self-employed contractor receives a CP503 (second notice of balance due). They intend to call the IRS “when things settle down.” Thirty days later, a CP504 arrives — a notice of intent to levy. They still don’t act. The IRS files a federal tax lien. Now the contractor’s credit is impacted, their bank account is exposed, and the window for a Collection Due Process hearing — which could have halted the levy — is closing fast.

That sequence took less than 90 days. And at no point did the IRS do anything unusual.

This is the contrarian claim worth stating plainly: the IRS isn’t the obstacle. The taxpayer’s unfamiliarity with IRS procedure is.

The enforcement system works exactly as designed. The problem is that it was designed for tax professionals to navigate — not individuals acting alone under financial stress. Understanding why conventional tax resolution approaches fail helps explain why so many taxpayers reach Stage 4 before they act.

What Does Actual Resolution Look Like — With Real Numbers?

Resolution is not a single outcome. It’s a matched pathway — the right IRS program for the specific financial profile of the taxpayer.

The three primary resolution pathways are:

| Resolution Pathway | Best For | Typical Timeline | Key Requirement |

| Offer in Compromise (OIC) | Taxpayers who genuinely cannot pay full liability | 6–18 months | Demonstrated inability to pay in full |

| Installment Agreement | Taxpayers who can pay over time | 30–90 days to establish | Sufficient income to cover monthly payments |

| Currently Not Collectible (CNC) | Taxpayers with no current ability to pay | 30–60 days to establish | Expenses exceed income; no available assets |

The IRS acceptance rate for Offers in Compromise has varied over the years — IRS statistics show acceptance rates typically ranging from 30–40% of submitted offers. That means more than half of OIC applications are rejected. The reason is almost always the same: the offer was submitted without a complete financial analysis that accurately reflects the taxpayer’s Reasonable Collection Potential (RCP).

RCP is the IRS’s calculation of how much it can realistically collect from a taxpayer over the remaining collection statute period, based on assets and future income. It is the single number that determines whether an OIC will be accepted or rejected — and most self-prepared offers get it wrong.

Consider this pattern: a small business owner three years into penalty accrual, with an original liability of $85,000 that had grown to $127,000 with interest and penalties, resolved through an accepted OIC at $11,200 — an 11-month process that required a complete financial disclosure, accurate RCP calculation, and persistent follow-up with the IRS examiner. The difference between $127,000 and $11,200 was not luck. It was documentation and process.

McCauley Law Offices has documented results of this kind repeatedly — including a $1.2 million liability reduced to $27,000, and cases where clients saved over $250,000. Those outcomes aren’t typical for every case, but they reflect what proper procedural navigation can achieve.

> Saving $100,000 on a tax debt isn’t a negotiating trick — it’s the result of knowing exactly which IRS program applies, exactly what documentation is required, and exactly when to submit it.

How Does Hiring a Tax Attorney Compare to Other Options?

This is where most people get stuck — not because the options are unclear, but because the tradeoffs are undersold.

Enrolled Agent vs. Tax Attorney: An enrolled agent is licensed to represent taxpayers before the IRS and can handle most resolution cases competently. However, enrolled agents cannot represent clients in federal tax court, cannot invoke attorney-client privilege in criminal tax matters, and have limited authority in cases where the IRS pursues civil fraud penalties. If your situation has any criminal exposure — unreported income, unfiled returns over multiple years, offshore accounts — you need an attorney.

DIY Resolution: The IRS does have self-help resources, and for simple installment agreements on modest balances, some taxpayers manage it. But the moment a lien is filed, a levy is threatened, or an audit is opened, DIY becomes a liability. The IRS representative you speak with is not your advocate. They are an enforcement officer doing their job.

Tax Resolution Companies (Non-Attorney): These firms advertise heavily and often charge significant upfront fees. Some are legitimate. Many are not. The Federal Trade Commission has taken action against numerous tax resolution companies for deceptive practices. The key distinction: a licensed tax attorney carries professional liability, bar oversight, and attorney-client privilege. A non-attorney resolution company carries none of those protections. What a tax attorney actually does that general advice leaves out is precisely this combination of legal authority, privilege, and procedural command that no other representative can replicate.

McCauley Law Offices operates as a tax attorney firm — not a resolution mill. That distinction matters when the IRS pushes back.

The Enforcement Escalation Framework: Knowing Where You Stand

The Enforcement Escalation Framework is a five-stage model for understanding where a taxpayer sits in the IRS collection sequence and what options remain at each stage.

- Stage 1 — Notice Phase: CP2000, CP501, CP503. Full range of options available. Best time to act.

- Stage 2 — Intent to Levy: CP504. Collection Due Process rights still active. OIC, CNC, and installment agreements fully available.

- Stage 3 — Lien Filed: Federal tax lien on record. Credit impact begins. CDP hearing window is 30 days from lien notice.

- Stage 4 — Levy Executed: Bank account or wages seized. Options narrow significantly. Immediate intervention required.

- Stage 5 — Enforcement Escalated: Referral to Department of Justice, criminal investigation, or seizure of physical assets. Attorney representation is not optional at this stage.

Use this framework when: you’ve received any IRS notice and need to understand urgency. Not when: you’re still in the filing phase with no outstanding liability — this applies to post-assessment enforcement only.

Most people who call McCauley Law Offices are at Stage 2 or Stage 3. The ones who wait arrive at Stage 4.

Who Is This NOT For?

Honest answer: not every tax problem requires a tax attorney, and not every taxpayer is a fit for the resolution programs described here.

If you owe less than $10,000, are current on filing, and simply need a payment plan — the IRS Online Payment Agreement tool may be sufficient. If your only issue is an unfiled return with no assessed liability yet, a CPA or enrolled agent may be the right first call.

McCauley Law Offices works best for taxpayers facing active enforcement — liens, levies, garnishments, audits, or multi-year debt with significant penalty accumulation. If your situation involves potential criminal exposure, substantial debt over $50,000, or business tax liability with trust fund penalties, that’s exactly the profile where hiring a tax lawyer pays for itself many times over.

Frequently Asked Questions

How long does it actually take to stop a wage garnishment? In most cases, a wage garnishment can be released within days of submitting a proper request to the IRS — but only if the right documentation accompanies it. An attorney who knows the specific IRS unit handling your case can accelerate this significantly. Without representation, the process can stall for weeks.

Will the IRS really negotiate with me, or is that just marketing? The IRS does negotiate — it has formal programs specifically designed for taxpayers who cannot pay in full. The Offer in Compromise program, installment agreements, and Currently Not Collectible status are all codified in the Internal Revenue Code. What the IRS won’t do is negotiate without complete, accurate financial disclosure. Incomplete submissions are rejected outright.

What happens if I just ignore the IRS notices? Ignoring IRS notices does not make the debt disappear — it eliminates your procedural options one by one. Each unanswered notice moves your case further down the enforcement escalation chain. By the time a levy is executed, several legal windows that could have stopped it have already closed permanently.

Can the IRS take my house? Yes. The IRS has the authority to seize and sell real property to satisfy a tax debt, though it is a last resort that requires internal approval. A federal tax lien filed against your property can also prevent you from selling or refinancing until the debt is resolved. Acting before a lien is filed is always better than acting after.

What’s the difference between a tax attorney and a CPA for IRS problems? A CPA is trained in accounting and tax preparation. A tax attorney is trained in tax law, negotiation, and legal procedure. For IRS audits, disputes, and enforcement actions, the legal authority and attorney-client privilege that comes with an attorney matters. For routine tax filing and planning, a CPA is often sufficient.

How much does tax attorney representation cost compared to what I owe? Attorney fees vary based on case complexity, but for taxpayers with significant debt — $50,000 or more — representation typically costs a fraction of what proper resolution saves. A case where $127,000 is resolved for $11,200 absorbs attorney fees and still produces a net savings that would have been impossible without representation.

What should I bring to a first consultation with a tax attorney? Bring every IRS notice you’ve received, your last three years of tax returns if available, any correspondence you’ve sent to the IRS, and a general sense of your current income and assets. You don’t need everything organized perfectly — the attorney’s job is to assess the situation and tell you exactly where you stand.

You Know What You’re Facing. Now Do Something About It.

If you’ve read this far, you’re not casually curious. You’re dealing with something real — a notice, a garnishment, a lien, or a debt that’s been growing while you’ve been trying to figure out your next move.

The next move is a conversation. Not a commitment. Not a payment. A conversation with a tax attorney who will tell you exactly where you stand, what options are still open, and what it takes to get the IRS off your back for good.

Call McCauley Law Offices for a free, risk-free case evaluation. Tell them where you are in the enforcement sequence. Find out what’s still possible. Every day you wait, one more option closes.

References

IRS Data Book — Annual IRS publication covering collections, enforcement statistics, and taxpayer compliance data.

IRS.gov — Official source for Offer in Compromise program guidelines, Collection Due Process procedures, and installment agreement eligibility criteria.

Internal Revenue Code (IRC) — Governing statute for all IRS enforcement authority, including levy, lien, and seizure provisions.

Federal Trade Commission (FTC) — Source for enforcement actions taken against deceptive tax resolution companies.